Buy Now Pay Later: Is it time to say bye-bye?

24 March 2023

Is the real threat to the poster-children of Buy Now Pay Later (BNPL) coming from rising interest rates and the attentions of regulators? Or will it be from the arrival of bigger, more trusted brands that can satisfy the craving of consumers for the instant purchase gratification they seek?

It’s been a week (or three) for BNPL players

It’s been hard to miss the stock market woes and industry vitriol leveled at the BNPL sector over the last few weeks.

BNPL boomed and was the darling of VCs during COVID-19 as ‘bored-at-home’ e-commerce shoppers took advantage of short-term financing options to spread the cost of both planned and spontaneous online purchases over multiple installments, usually with zero interest added.

The story of BNPLs recent troubles started in the US with Affirm (NASDAQ: AFRM) on February 8th.

Their current $3.8billion valuation was already 84 percent lower than the $24billion they enjoyed shortly after their 2020 IPO. Then they missed Q2 2023 fiscal earnings, sending their stock price down 18 percent in a single day.

On the last day of February, Europe got in on the act too. Swedish unicorn Klarna had watched their valuation drop from US$46bn to US$6.7bn in twelve months and reported 2022 accumulated losses of $1bn.

The Asia Pacific (APAC) region didn’t want to get left out either.

Hot on the heels of early February’s collapse of Australia’s Openpay (AXS:OPY) leaving debts of AUD$18.2 million, ZIP (AXS: ZIP) kicked off March by acknowledging it was time to tighten purse strings and announced their exit from India, the Philippines, Turkey, Czech Republic, South Africa, Poland, Singapore, the UK, Mexico and the Middle East. In fact, they exited 10 out of the 14 global markets they operated in. This move, against the news of a backdrop of AUD$240 million loss in 2022, was accompanied by a share price that has plummeted 95 percent since Feb 2021 (formerly trading at $12 AUD compared $0.5 AUD this week).

Temporary trouble or a terminal tipping point?

BNPL providers are victims of two universal trends – the decline in fintech valuations in anticipation of a tough global economy and the slowly deflating bubble of the COVID-19 induced e-commerce boom. These are significant macro-economic factors but there’s a lot more contributing to BNPL’s rocky start to 2023.

Global inflation squeezes BNPL providers at both ends

Most of the current BNPL players flourished during an extended period of almost uniquely low borrowing costs. If your business model depends on borrowing money to lend out at zero interest, any increase in borrowing rates inevitably and immediately impacts profitability. High inflation also threatens consumer discretionary spending. Luxury and ‘want-not-need’ purchases, the heartland of BNPL’s early growth, have been the first to go as consumers worry about rising costs.

The spectre of regulation is looming

The UK government’s Valentine’s day gift to the industry was the launch of a public consultation on legislation to regulate BNPL, giving the Financial Conduct Authority (FCA) powers to authorize operators and their activities. Similar initiatives are underway in the US and across Europe amid concerns that the low barrier to entry offered by BNPL makes it too easy for people to accumulate debt that they cannot ultimately afford to pay off.

Everybody wants in on the BNPL action

Pure-play fintechs in the BNPL space are being challenged on several fronts.

‘Big Credit’ is waking up to the opportunity.

In 2022 Visa launched ‘Visa Ready’ and Mastercard launched ‘Mastercard Installments’, their own BNPL offerings. Both have the advantage of already established, large global acceptance networks e.g., Mastercard has over 90 million merchants compared to Affirm’s 29,000. They also have powerful global brand recognition leaving new BNPL players in an unfair fight on two fronts: building their B2B brand presence while also building trust and demand in B2C markets.

And let’s not forget the long-awaited ‘Apple Pay Later’ is currently being tested by employees and will be launched soon according to senior sources at Apple.

Tech startups are chasing the money too. SaaS platforms like Amount and Jifiti are offering an alternative to partnering with an established BNPL fintech by building a technological bridge between a portfolio of bank partners and brands that want to integrate BNPL into their branded shopping experiences (e.g. Credit Agricole and IKEA France).

That is a lot to contend with in already challenging economic times.

But is it all bad news for BNPL?

The irony behind all the industry nay-saying is that you’ll be hard pressed to find any industry pundit that does not see a strong, if evolved, future for BNPL as a concept.

Demand is only going in one direction.

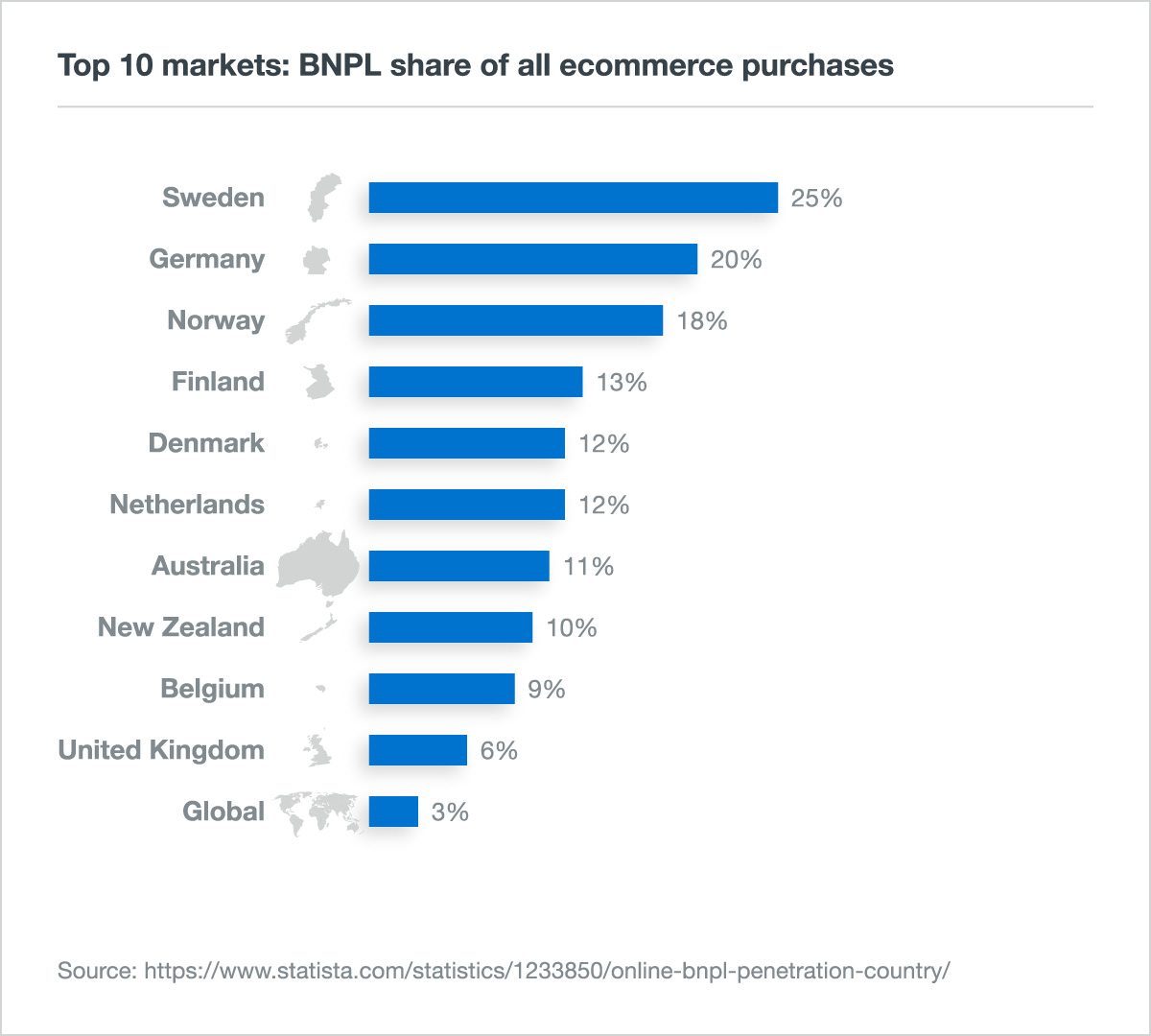

BNPL accounts for a significant amount of e-commerce purchases already e.g, 25 percent of all ecommerce payments in Sweden and 20 percent in Germany.

While both Europe and key APAC markets Australia and New Zealand are ahead of the US (ranked 14th with 4 percent of e-commerce purchases via BNPL), Bain and Co. estimated that US BNPL accounted for US$49 billion of consumer e-commerce purchases in 2021 and will reach US$265 billion in the next five years, generating a US$4 billion incremental fee-based revenue stream for the brands offering BNPL.

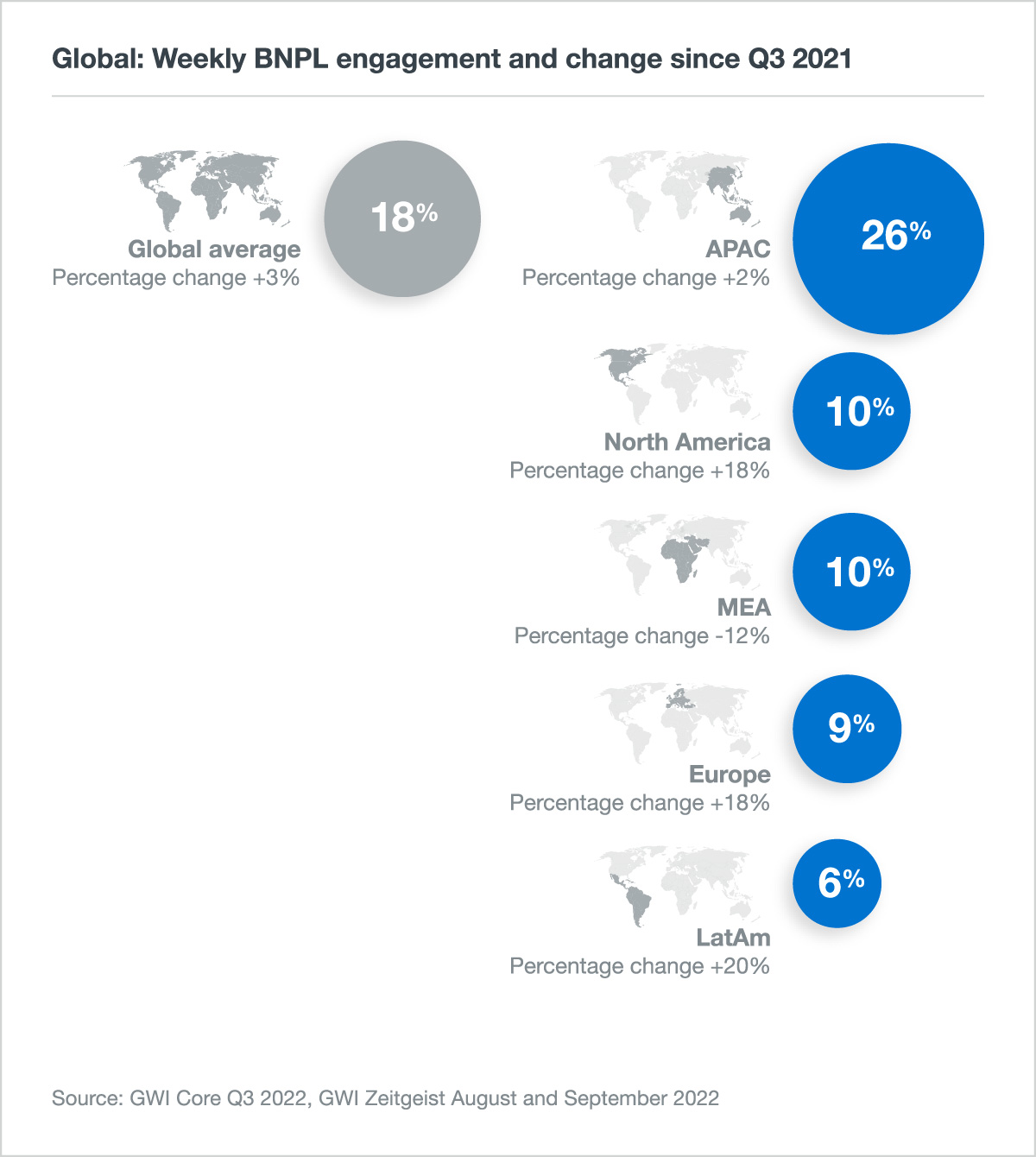

Research among 15,578 consumers across 12 countries shows that 18 percent of the online population aged between 16-64 had used a BNPL service within the last week, an increase of 3 percent compared to the same time last year. APAC, while still a little behind other regions at 6 percent had seen 20 percent growth compared to 2021 levels.

The customer wants what the customer wants

Putting aside inflation-driven blips to consumer spending, the need for instant gratification is growing in significance for both millennials and GenZ in particular.

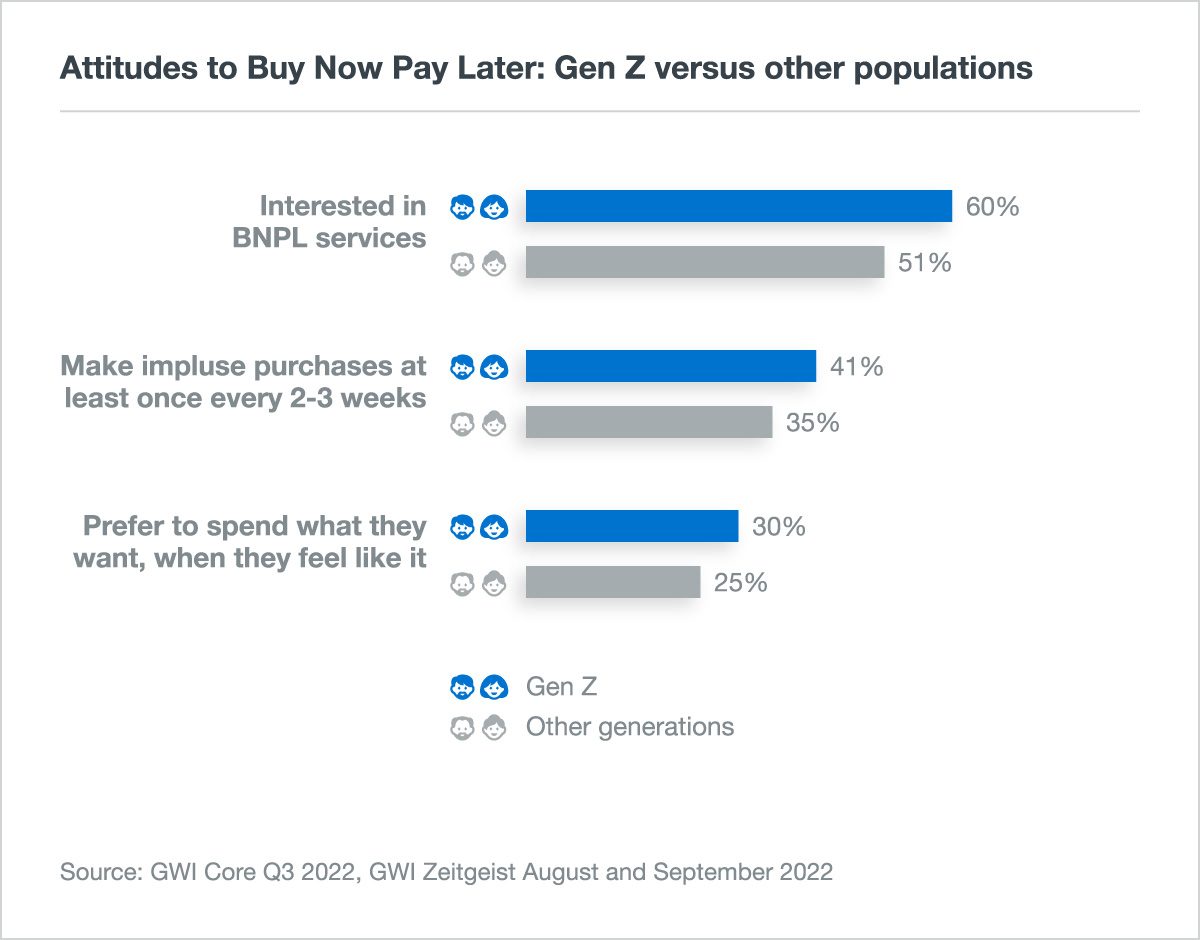

In the same 12-country study, 41 percent of global GenZ make impulse purchases every two to three weeks compared to 35 percent of other generations. Almost a third (30 percent) say that they prefer to spend what they want, when they feel like it and 60 percent are explicitly interested in BNPL.

A 50-country study of over 250,000 respondents revealed that while other generations were showing evidence of pulling back on major purchases, GenZ expenditure on discretionary items was expanding. Between Q3 2021 and Q3 2022 GenZ purchases of concert tickets had gone up 44 percent, flights and travel by 23 percent and experiences like spas or day trips had increased 15 percent. Similar patterns emerged for millennials.

In response to two years in lock down, the digital generations are placing significantly more value on their right to be spontaneous – a perfect storm for a strong future demand for BNPL.

It’s BNPL, but not as we know it

BNPL isn’t going anywhere because consumers want what it delivers – instant gratification in a relatively low-risk financial environment.

It is not going anywhere because brands want it, not only to enhance their customer experiences but as a revenue stream.

Most importantly, the future of meaningful financial experiences is contextual and embedded. BNPL (done well) personifies this.

The real question isn’t about the future of BNPL, but the future of BNPL providers.

The winners will be those with a clear and compelling B2B2C brand story. Those who can attract a wide range of merchants and can secure the trust of their merchants’ customers.

In a competitive market, BNPL providers first need to have a highly differentiated B2B brand. They need a compelling story, deep knowledge of the markets they want to serve, a compelling business case to take to potential partners and a financial model that delivers a win-win-win for platform, merchant and shopper alike.

Those willing to partner with brands and allow white labelling will open new opportunities so retailers can offer a consistently branded experience that consumers already trust.

There’s nothing to be gained by hanging around waiting to be regulated, leaders will be those that voluntarily educate borrowers, have a content strategy in place to address gaps in financial literacy and tighten up their acceptance criteria to ensure that people who use their service can afford the debt they are accumulating.

Fair, open, and transparent customer experiences will win out.

The future might need to look a little different and it might take some creative B2B2C brand strategy but the B in BNPL still definitely stands for buy, not bye.

Blog originally featured on Finextra: https://www.finextra.com/the-long-read/621/buy-now-pay-later-is-it-time-to-say-bye-bye